GAMBRELL FINANCIAL NEWS

YOUR TRUSTED FINANCIAL info center

We’ve been working at our best to ensure our clients’ financial future, and to provide the best financial services possible. We stand for quality and credibility, so you could be sure about our work.

TOP-RATED FINANCIAL NEWS

Don’t have time to read, you can listen to our podcast at: https://www.redzonetoolbox.com/

Have a topic you would like more clarity on send us an email: info@gambrellfinancial.com

Retain Key Employees w/A Bonus Plan

Overall, the Section 162 Executive Bonus Plan is an effective way to retain key employees and provide an additional layer of benefits. The plan is straightforward to implement and can be customized for each executive. The employee ownership of the policy and policy values provides financial flexibility, and the tax-deferred growth on accumulations and tax-free death benefit make it an attractive option.

- Retain Key Employees

- Payback Agreement

- The employer may enter into a side agreement with the employee that states if the employee leaves the employer’s employment prior to a certain specified date, the employee will be required to pay back the bonuses received.

- Vesting Schedule, The employer can provide a vesting schedule whereby if the employee leaves the company prior to full vesting, the employee will be required to pay back the unvested amount.

- Tax Impact Under a Section 162 Executive Bonus Plan, the employee takes each year’s bonus into taxable income as received or when the premium is paid by the company. Some companies will gross-up or pay an additional bonus for projected income taxes and payroll taxes attributable to the bonus. Since the employee owns the life insurance policy or non-qualified deferred annuity, they will have access to policy values.

- The only exception to the bonus being deductible is if the IRS would rule that the employee’s total compensation is unreasonable. If that is the case, the employer would be limited in how much they can deduct but the employee would still take all of the compensation into taxable income.

- Employer selects which executives they wish to benefit

- Employer chooses benefit level and can customize for each executive

- 162 Executive Bonus Plan easy to implement and administer

- No administration other than regular payroll

- Bonuses may be fully deductible to employer under IRC 162

- Rewards and retains Key Employees

- Plan can be terminated by company at any time

- Employee owns the policy and policy values

- Employee gets to name beneficiaries

- Accumulating values can be accessed by employee

- Tax-deferred growth on accumulations

- Tax-free death benefit in case of life insurance

- Life insurance can benefit survivors and pay estate costs

- Cash values available for emergencies

- Cash values may be used to supplement retirement income

“Life Insurance You Don’t Have To Die To Use”

“Life Insurance You Don’t Have To Die To Use”

With this kind of plan, you get to be the beneficiary of your own policy. Many Americans over the age of 30 are on some kind of prescription drug.

Life Time Retirement Income Guaranteed*

Guarantee yourself a lifetime of income. Protect your principle- keep your money safe

Do you have a plan to never outlive your retirement money?

Did you know that an FIA, Fixed Index Annuity can provide you with an income you can never outlive guaranteeing you never lose any of your money!

An FIA can provide you with the peace of mind retirement you deserve. A fixed indexed annuity allows you to have an insurance contract that protects you against outliving your retirement nest egg. If you are in the “Retirement Redzone” age 50-75 you can’t afford another “Stock Market Loss”.

What happens if you are 62 and the market crashes? Do you think it’s realistic to recover a 44% account value drop 3 years before retirement? What if the market crashes after you’ve been retired for 5 years. Will your health allow you at the age of 70 to go back into the workforce?

When the market crashed in 2002 it took 13 years just to make a 1$. It took 13 years before recovering what you lost plus $1.

It’s mathematically impossible to recover a 20% – 44% loss in account value while also withdrawing money to live on!

With an FIA, your contract account balance doesn’t decrease during a time of market loss. You will not earn any interest during a market loss but most importantly you will never lose any money! When the market recovers the interest crediting will continue.

For example: In a typical market account, let’s say you have 1 Million. For simple math let’s also say you have 1 Million in an FIA Fixed Index Annuity.

If the market drops 44% but you only lose 35% this means your 1 Million account value drops to $650,000.

With the Fixed Index Annuity, you have what’s called a ZERO Percent floor. This means the least amount of money you will earn during a market decline is zero percent.

Using the same scenario as above, if you have a 1 Million account value and the market drops the same 44%, guess what happens?

You’ll still have the same 1 Million account value because you can’t lose any money due to market losses.

The price for having this retirement safety net is this…. You can’t have unlimited gains if you remove the risk of market loss.

With a Fixed Index Annuity, you have what’s called an Annual reset or annual point to point crediting.

At the end of each term your money is locked in place so it can never go backwards due to market losses.

You can only go up from the amount of interest credited based upon a percentage of market gains, and you never go back from a market loss. Every term, your contract account value gets locked into place, and it can’t go into reverse

The amount of interest in a fixed index annuity will be limited based upon caps and participation rates as defined in the annuity contract.

In exchange for receiving an income guaranteed for the rest of your life, the insurance company will limit the unlimited interest you could earn in the market, that way they can guarantee you’ll never lose any money!

Because a Fixed Index Annuity is an Insurance product and doesn’t directly invest in the market. The insurance company using what’s called mortality credits along with other crediting options, are able to provide you with a higher payout dollar per dollar than what you would receive with a typical market account.

In other words, you don’t have to accumulate the same amount of money in a FIA to equal the same payout as a typical market account.

Assuming the 4% Rule you would need a 1 Million account value at retirement in order to receive $40,000 of income with an 88% – 92% chance of not running out of money.

With a Fixed Index Annuity and as a result of mortality credits you would only need $600,000 to provide you with the same $40,000 of income while also eliminating the possibility of you running out of money.

With a Fixed Index Annuity, even if the account balance goes to zero, you will continue to receive the same income forever, guaranteed!

A Fixed Index Annuity isn’t for everyone, and you shouldn’t move all of your money to an FIA.

My rule of thumb is this…. The amount of money you need to pay the bills, keep food on the table, pay for transportation cost along with medical cost, the monies needed to ensure these basic needs are covered, should be guaranteed with an FIA! The monies you don’t need to cover basic needs can be left in market products.

Guarantee the core and have fun with the rest.

Obviously the scenario used in this example is not a representation of your situation. The only way to determine if any of the information would benefit you is to schedule a one-on-one face-to-face meeting with myself or a member of my team.

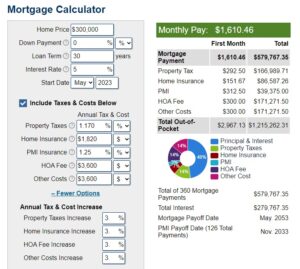

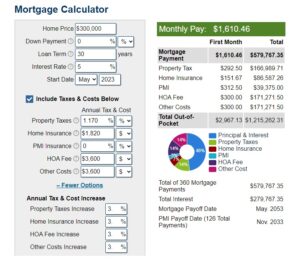

True Cost Of Home Ownership

Our unique Health Insurance Savings Strategies has helped small business owners, families and individuals save millions of dollars in health insurance premiums using our “Gap Insurance For Health Insurance Strategies. You can even pay for your individual health insurance with tax free money!

With PMI

$300,000 Home assuming zero down.

NO PMI

$300,000 Home assuming zero down.

After 30 years with an average growth of 3% the home would be worth… $728,178.74

FIA - Annual Point-to-Point with a Cap

FIA – Fixed index annuities offer the possibility of capital gains during favorable market conditions, while simultaneously eliminating downside risk during unfavorable ones.

Point-to-point serves as a straightforward interest crediting strategy utilized to calculate growth within an index annuity. Annual point-to-point provides a suitable option for investors seeking to minimize mid-year market volatility.

This technique involves the insurance company comparing the index price at the end of the index term to its price at the beginning of the term for one year.

In the event of a price increase, the interest credited to the contract equals the percentage of the index price increase, up to a cap or participation rate. Conversely, interest credited is zero percent in the event of a decrease, thereby precluding any loss. Caps tend to fluctuate up and down over the course of an annuity contract’s duration, often tracking treasury rates.

Potential buyers should ascertain the contractual minimum caps and participation rates before purchasing an annuity.

Some fixed index annuities offer uncapped crediting strategies, where there is no limit to how much can be earned. However, there may be a spread, a percentage deducted before gains are credited. In this example, we have the same 20% index gain with 150% participation rate and a 5% spread. In this case, we are participating in one and a half times the index gain – or 30% – minus the 5% spread – so we would be credited with 25%. If the index was up 4%, we would participate in 6% growth, and after the 5% spread, we would be credited with 1% gain.

Charitable Remainder Trusts (CRTs)

Charitable Remainder Trusts (CRTs) funded by insurance-based Wealth Replacement Trusts are a strategic approach to reducing significant long-term capital gain taxes. The Health Care Act of 2010 implemented a 3.8% tax on investment income for single individuals and married couples filing jointly, earning over $200,000 and $250,000 respectively. The proposed solution is to contribute some or all of the stock from the asset the individual intends to sell to a charitable trust. The proceeds from the sale of the stock in the charitable trust are tax-free, allowing the individual to invest more money in the charitable trust, increasing their income and paying out income to beneficiaries.

The contribution generates a charitable tax deduction that can offset ordinary income or other capital gains from the remaining stock that is not donated to the charitable trust. The size of the deduction depends on the age of the beneficiary, the amount of the trust payout, and the type of property contributed. The charitable tax deduction can be used within the contribution year, with a five-year carry-forward of any unused deduction.

The increased income from the charitable trust allows for the contribution of a portion of the income to an irrevocable life insurance wealth replacement trust, benefitting children or loved ones by replacing the value of the asset or a portion of the value. The Signature Guaranteed Universal Life Policy or Signature Performance Indexed Universal Life Policy are potential candidates for funding the trust.

Selling a business or significant asset through this transaction reduces substantial taxes, shelters sales proceeds, and provides a more substantial income than would have been available after taxes. This approach also enables individuals to contribute to their favorite charity through a significant benefit at their death. To avoid being taxed on the proceeds personally, the individual must contribute the stock to the charitable trust before receiving a sales contract on the business.

For those considering selling their business or a large block of publicly traded stock with charitable interests, this strategy can help to accomplish their life goals while benefiting their chosen charity and loved ones.

Social Security Income. How it works!

The Social Security program was established to provide a financial safety net for retired and disabled workers and their families in the aftermath of the Great Depression. It is mandatory and requires most wage earners to contribute a percentage of their annual income to support the program, with 6.2% of earned income being withheld for Social Security and an additional 1.45% for Medicare.

Employers also contribute an equal amount. Social Security benefits are available to retired, disabled, and surviving workers and their families.

Individuals born before 1938 are eligible to collect full Social Security benefits at age 65, while those born after 1938 will experience a gradual increase in the Normal Retirement Age (NRA) from age 65 to 67. Surviving spouses are entitled to benefits based on their deceased partner’s earnings history unless they would receive more based on their own history.

Once individuals begin receiving retirement benefits, they may need to include them in their taxable income reported to the IRS. Federal income tax on Social Security benefits is owed if the total income for the year, including half of Social Security and tax-exempt earnings, is greater than $32,000 ($25,000 for single taxpayers). The IRS provides a worksheet to calculate the amount of taxable income.

It is essential to maintain an accurate record of Social Security earnings. This record can be obtained from the Social Security Administration (SSA) by filling out Form 7004 and mailing it to the SSA. If errors are discovered, evidence must be provided for correction. It is recommended to check earnings records every three years to catch and correct any issues early on.

This material is for informational purposes only and should not be construed as tax, legal, or investment advice. While the information is believed to be reliable, individual situations can vary, and professional advice should be sought when making decisions.

The Advantages of Delaying Social Security Benefits

The Advantages of Delaying Social Security Benefits

The decision to delay claiming Social Security benefits can be a smart financial move, but it is important to consider the statistics and your individual circumstances. Assuming you have earned the maximum level of Social Security benefits throughout your career, waiting to claim benefits can result in significant increases in your monthly check.

For example, if you were to claim benefits at age 62 in January 2022, your monthly retirement benefit would be $2,364. Waiting until age 67 to claim benefits would increase your monthly check by nearly 51% to $3,568. And if you were to delay claiming benefits until age 70, your monthly check would be over 17.5% higher at $4,194.

However, it is important to consider what your cumulative benefits will be. At age 76, the cumulative benefits for claiming at age 67 will exceed those for claiming at age 62. And at age 87, the cumulative benefits for claiming at age 70 will top those for claiming at age 67.

Additionally, the average lifespan for men in the U.S. is 75, and 81 for women. For many Americans, delaying claiming benefits until age 70 may not pay off because they will not live long enough to see the increased benefits. However, for those who live to age 65, the average life expectancy is another 19.1 years for males and another 21.7 years for females, which may change the decision-making dynamics.

Considering the time value of money, even if you do not need Social Security benefits at age 67, you could claim them and invest the money in a low-risk alternative such as Treasury bonds. This could further justify delaying claiming benefits.

Ultimately, the decision to delay claiming Social Security benefits should be based on individual circumstances and factors such as life expectancy, financial needs, and investment opportunities.

How to Transfer a Family Business to the Next Generation

The longevity of a family business can be ensured by establishing a clear and concise plan for its future, including the transfer of ownership to the next generation. This strategy is aimed at preserving the integrity of the business and avoiding unexpected tax liabilities. There are four methods to transfer a business to children: outright gifting in a will, gift giving, selling the business, and transferring the business to a trust.

The use of a grantor trust is advantageous because it avoids various taxes on assets and interest payments.

In situations where multiple children are involved, it is important to plan ahead for unforeseen events like death or incapacitation. The use of a Buy-Sell Agreement can ensure shares are reassigned legally if a business partner dies or is incapacitated. This legal contract provides an indirect control mechanism for the original owner and facilitates the transfer of remaining shares to children working in the family business.

In cases where children have varying levels of interest in the business, it is crucial to tailor the transfer plan to each child’s level of engagement. The use of life insurance to purchase remaining shares from the estate is an effective way to equalize the estate. The owner should also consider taking liquid assets and putting them into a deferred annuity to optimize tax savings.

In summary, the transfer of a family business requires a thorough and precise plan to ensure a successful transfer to the next generation. The available options can be tailored to the specific needs of the business, the family, and their goals.

Strategic Business Planning Buy-Sell Planning

Strategic Business Planning Buy-Sell Planning

Strategic Business Planning Buy-Sell Planning

The continuity of any business depends on a well-conceived plan for the transfer of ownership in the event of death, disability, or retirement of the owner. Unfortunately, many entrepreneurs have yet to develop a viable succession plan for their enterprises, leaving their future in jeopardy.

A proficient Buy-Sell Agreement can provide an orderly transition of ownership from one proprietor to another. However, a funding mechanism must be established to cover the withdrawing owner’s share of the business. American National’s life insurance products offer cost-effective and tax-efficient methods of financing Buy-Sell Agreements.

Business Planning

The implementation of life insurance and annuities may offer various solutions for business owners. Life insurance policies may be utilized to entice promising talent, safeguard the business against the loss of key staff members, or engender loyalty among employees by providing financial security to their loved ones. Additionally, life insurance and deferred annuities can furnish supplementary benefits to valued personnel.

Understanding Capital Gains Tax

Understanding Capital Gains Tax

A Comprehensive Overview of Capital Gains Taxation

The Jobs and Growth Tax Relief Reconciliation Act of 2003 offers taxpayers the chance to reduce their taxes by generating long-term capital gains or acquiring dividend income. However, it is important to note that “sunset provisions” have been put in place, which means that tax rates on capital gains and dividends may increase again if Congress does not act to extend the rates. As of now, the lower rates are only valid until 2010.

The Taxation of Long-Term Capital Gains

Under this act, the tax rate for most taxpayers on net capital gain cannot exceed 15%, while taxpayers in the 10% and 15% tax rate brackets are subject to a 5% tax rate for property sold or otherwise disposed of after May 5, 2003 (and installment sale payments received after that date). This reduced rate applies for both the regular tax and the alternative minimum tax.

(Note: Higher rates that apply to unrecaptured section 1250 gain, collectibles gain, and section 1202 gain remain unchanged.)

The Tax Treatment of Capital Losses

If you incur losses from selling a capital asset, you may deduct those losses to the extent they equal capital gains from selling other assets. If your losses exceed your gains, you can only deduct up to $3,000 ($1,500 if married and filing separately) of capital losses in a tax year against other income on Form 1040. You may carry losses forward and continue to deduct $3,000 ($1,500 if filing separately) annually against other income until your losses are exhausted.

It is important to note that the information discussed herein is for general illustration and informational purposes only. It should not be construed as tax, legal, or investment advice. Although the information has been gathered from reliable sources, individual situations may vary, and as such, it should be relied upon only when coordinated with professional advice.

Longevity Risk Avoid Running out of Money During Retirement

Longevity Risk Avoid Running out of Money During Retirement

Longevity Risk: Avoid Running out of Money During Retirement by Using an FIA

Are you nearing retirement age and worried about the risk of running out of money? If so, you are not alone. For many Americans, the thought of outliving their retirement savings is a major concern. But the good news is that there is a solution to this problem: a Fixed Index Annuity (FIA).

As an expert in the retirement planning industry, I have seen firsthand the impact that longevity risk can have on retirees. Sequence of returns risk, sequential withdrawal risk, living too long, outliving retirement income, and stock market losses during retirement are all factors that can contribute to the risk of running out of money. But with an FIA, you can protect your retirement income and avoid this risk altogether.

So, what exactly is an FIA? It is a type of annuity that allows you to participate in the potential growth of the stock market while protecting your principal from market losses. With an FIA, you can lock in gains during good years and never lose money during bad years. This means that you can enjoy the peace of mind of knowing that your retirement income is safe, regardless of what happens in the stock market.

But the benefits of an FIA don’t stop there. In addition to protecting your retirement income, an FIA can also provide you with a lifetime income stream. This means that you can receive guaranteed income payments for as long as you live, ensuring that you never run out of money during retirement.

And unlike other retirement income strategies, an FIA does not require you to sacrifice growth potential for safety. With an FIA, you can benefit from the upside potential of the stock market without exposing your retirement income to market risk.

So, why should you consider an FIA as part of your retirement income plan? Simply put, it provides the peace of mind and financial security that retirees need to enjoy their golden years without worrying about money. With an FIA, you can protect your retirement income from the risk of running out of money, and enjoy the retirement lifestyle that you have always dreamed of.

To get started with an FIA, all you need to do is contact a retirement planning expert like me. I can help you assess your retirement income needs and create a customized plan that includes an FIA. Don’t wait until it’s too late – take control of your retirement income today and enjoy the peace of mind that comes with knowing you are protected from longevity risk.

To sum it up, avoid running out of money during retirement by using an FIA. Protect your retirement income from the risk of sequence of returns, sequential withdrawal, living too long, outliving your retirement income, and stock market losses with an FIA. Contact a retirement planning expert like Mel Gambrell to create a customized plan today. Don’t wait until it’s too late – take control of your retirement income and enjoy the peace of mind that comes with knowing you are protected from longevity risk.

How to Take Portfolio Withdrawals in a Market Downturn

How to Take Portfolio Withdrawals in a Market Downturn

When it comes to investing, market downturns can be nerve-wracking. Investors may become anxious about market volatility and may be tempted to withdraw their portfolio. However, withdrawing your portfolio during a downturn can be a big mistake as it can lead to significant losses. In this article, we will discuss how to take portfolio withdrawals in a market downturn, providing tips and strategies to help investors make informed decisions.

Have a Withdrawal Strategy in Place

If you’re worried about a market downturn, it’s important to have a withdrawal strategy in place. This means having a plan for how much money you will withdraw and when you will do it. Having a plan in place will help you avoid making emotional decisions in the heat of the moment. Consider working with a financial advisor to help create a customized withdrawal strategy based on your goals and risk tolerance.

Rebalance Your Portfolio

During a market downturn, it’s common for some investments to perform better than others. Rebalancing your portfolio will help you stay diversified and minimize losses. Rebalancing involves selling investments that have increased in value and reinvesting the proceeds in investments that have decreased in value. This strategy can help you maintain a balanced portfolio and mitigate risk.

Consider Tax Implications

When withdrawing money from your portfolio during a market downturn, it’s important to consider tax implications. Withdrawals from a traditional IRA or 401(k) are typically subject to income tax, while withdrawals from a Roth IRA are tax-free. Additionally, selling investments at a loss can be used to offset capital gains and potentially lower your tax bill. Consult with a tax professional to help you navigate these complex tax issues.

Focus on Long-Term Goals

It’s important to remember that investing is a long-term strategy. While market downturns can be stressful, it’s important to focus on your long-term goals. Avoid making rash decisions based on short-term market movements, as this can lead to significant losses. Instead, stick to your investment plan and remain disciplined.

In conclusion, taking portfolio withdrawals during a market downturn can be a complex and challenging process. It’s important to have a strategy in place, rebalance your portfolio, consider tax implications, and focus on long-term goals. By following these tips and strategies, investors can make informed decisions and mitigate losses during times of market volatility.

LIRP – The Life Insurance Retirement Plan

Understanding LIRP – The Life Insurance Retirement Plan

The Life Insurance Retirement Plan (LIRP) is a unique financial tool that can help individuals secure their retirement while providing them with protection during their working years. LIRPs are becoming increasingly popular in the financial world as more people recognize the benefits they can offer.

What is a LIRP?

A LIRP is a hybrid financial product that combines the benefits of a traditional life insurance policy with those of a retirement plan. It is a cash value life insurance policy that is designed to provide a stream of tax-free income during retirement.

How does a LIRP work?

The structure of a LIRP is fairly simple. A policyholder buys a life insurance policy, paying a premium each year. The premium payments are invested and grow over time, building up a cash value within the policy.

The cash value can be accessed tax-free through withdrawals or loans during the policyholder’s lifetime. At the time of death, the beneficiaries receive the death benefit, which is typically tax-free as well.

Benefits of a LIRP

One of the primary benefits of a LIRP is the tax-free income it provides during retirement. Unlike traditional retirement plans such as 401(k)s or IRAs, the money withdrawn from a LIRP is not subject to income tax. This can be a significant advantage, particularly for individuals in higher tax brackets.

Another benefit is the flexibility a LIRP can offer. Unlike traditional retirement plans, there are no limits on how much can be contributed each year. This can be particularly beneficial for individuals who have already maxed out their contributions to other retirement plans.

Additionally, LIRPs offer protection against market downturns and other financial risks. The cash value within the policy is guaranteed to grow each year, regardless of market conditions. This can provide peace of mind for individuals who are concerned about the volatility of other investments.

Risks of a LIRP

The potential for the policy to lapse if the policyholder is unable to make the premium payments. If this happens, the policy may lose its tax-free status and the cash value within the policy may be forfeited.

Finally, LIRPs are not for everyone. They are best suited for individuals who are already maxing out their contributions to other retirement plans and who are comfortable with the risks associated with these products.

Conclusion

A LIRP can be a powerful tool for individuals who are looking to secure their retirement while also providing protection during their working years. Like any financial product, it is important to do your research and understand the risks and benefits before making a decision. With the help of a financial advisor, you can determine if a LIRP is the right choice for your retirement plan.

HECM Housing wealth

Don graves Speaks On HECM’s

Don Graves, RICP®,CLTC® and Certified Senior Advisor, CSA is the president and founder of the Housing Wealth Institute, an Author, and Instructor of Retirement Income at The American College of Financial Services. He is considered one of the nation’s leading educators on incorporating housing wealth into retirement income planning.

Don Graves has several Books available be sure to check them out!

Dr. Wade Pfau Answers 7 Questions about the Newly Restructured Reverse Mortgages

Dr Wade Pfau: Small Changes using Reverse Mortgages Can Produce Dramatic Portfolio Results

The Widow Who Can't Stop Working | Reverse Mortgage Case Study

The Widow Who Can't Stop Working (Part 2) | Rightsizing

Sell Your Home and Buy TWO with a Reverse Mortgage | Steve Parrish, JD and Don Graves Discuss.

Four Time Bombs of Retirement | Can a Reverse Mortgage Help | Chapter Guide

Roth Conversion Strategies Using Reverse Mortgages | 5 Strategies | Chapters Included

Getting to the Zero Tax Bracket - Part 1 | Don Graves interviews David McKnight

Getting to the Zero Tax Bracket - Part 2 | Don Graves interviews David McKnight

Wade Pfau on ‘Sequence of Inflation Risk’, the 4% Retirement Withdrawal Controversy, and More

Using Reverse Mortgages to Manage Sequence and Market Risk

More On Don Graves & Contact Info

Don Graves, RICP®,CLTC® and Certified Senior Advisor, CSA is the president and founder of the Housing Wealth Institute, an Author, and Instructor of Retirement Income at The American College of Financial Services. He is considered one of the nation’s leading educators on incorporating housing wealth into retirement income planning.

NMLS 142267 Don has been quoted in Forbes Magazine, featured on PBS-sponsored shows and recognized as one of the American College’s Top 11 Retirement Income leaders you need to read. His book: Housing Wealth: 3 Ways the New Reverse Mortgage Is Changing Retirement Income Conversations reached the Amazon #1 spot for New Releases in the Financial Services category in its 3rd week online. As both an educator and a skilled practitioner, Don has a unique perspective that very few share, and as a Retirement Income Certified Professional (RICP®), Long Term Care Specialist CLTC® and Certified Senior Advisor, he understands the powerful principles and strategies regarding retirement income planning, its design, intent, risks and limitations. He is a sought-after professional speaker, and his workshops are helping retirees across the country to grow their practices.

To find out more about reverse mortgages or how to work with Don Graves and his team please, go to https://hecmadvisorsgroup.com/contact... or if you have a question please email us at askdongraves@gmail.com If you are a consumer and would like a customized reverse mortgage illustration, please go to http://www.reversemortgageintake.com/ For More About Don Graves LinkedIN: https://www.linkedin.com/in/askdongra… Facebook: https://www.facebook.com/AskDonGraves Twitter: https://twitter.com/AskDonGraves YouTube:  / askdongraves

/ askdongraves

NOTE:

I highly recommend Don Graves along with using HECMs to enhance your retirement outlook.

The retirement income planning stratgies I help my clients implement includes the use of HECMs, however I’m not a mortgage loan professional. When it comes to the implementation of an HECM, Don Graves & his team will take good care you.

Contact my office today and request an appointment with Don Graves & his team of HECM professionals. info@gambrellfinancial.com

YOUR TRUSTED FINANCIAL info center

We’ve been working at our best to ensure our clients’ financial future, and to provide the best financial services possible. We stand for quality and credibility, so you could be sure about our work.

TOP-RATED FINANCIAL NEWS

Don’t have time to read, you can listen to our podcast at: https://www.redzonetoolbox.com/

Have a topic you would like more clarity on send us an email: info@gambrellfinancial.com

That 401(k) match isn’t just free money, 3% could buy you two years of retirement

Maximizing Your 401(k) Match: How 3% Could Buy You Two Years of Retirement

As an employee, contributing to your 401(k) plan is one of the best ways to save for retirement. But did you know that your employer’s matching contribution can significantly increase your retirement savings? In fact, a 3% match could mean the difference between retiring comfortably and having to work well into your golden years.

Understanding the 401(k) Match

Your 401(k) match is the amount that your employer contributes to your retirement savings account based on the amount you contribute. For example, if your employer offers a 3% match and you contribute $5,000 to your 401(k) in a year, your employer will contribute an additional $150.

It’s important to note that many employers require employees to contribute to their 401(k) plan in order to receive a match. This is known as a “vesting period” and can range from immediate vesting to several years before you are fully vested in your employer’s matching contributions.

Why Your 401(k) Match Matters

Your employer’s matching contribution is essentially free money that can significantly increase your retirement savings. But the impact of your 401(k) match on your retirement depends on how much you contribute and how long you save.

For example, let’s say you contribute $10,000 per year to your 401(k) and your employer offers a 3% match. Over 30 years, your employer’s matching contributions would add an additional $90,000 to your retirement savings. Assuming a 6% annual rate of return, this could increase your retirement savings by over $300,000.

But the impact of your 401(k) match on your retirement savings is even more significant if you start saving early. For example, if you start saving $5,000 per year at age 25 and receive a 3% match from your employer, you could have over $2 million in retirement savings by age 65. This is assuming a 6% annual rate of return, and no additional contributions or employer matches after age 35.

How to Maximize Your 401(k) Match

Maximizing your 401(k) match is key to maximizing your retirement savings. Here are some tips to help you make the most of your employer’s matching contribution:

Contribute the maximum amount allowed. The maximum contribution limit for a 401(k) in 2021 is $19,500, with an additional $6,500 catch-up contribution allowed for those over age 50.

Start saving early. The earlier you start saving, the more time your retirement savings have to grow.

Consider increasing your contribution over time. Even small increases in your contribution rate can make a big difference in your retirement savings over time.

Make sure you are fully vested. If your employer requires a vesting period for their matching contributions, make sure you understand the terms and are fully vested before leaving your job.

In conclusion, your employer’s matching contribution to your 401(k) is not just free money, it’s an investment in your retirement. By maximizing your 401(k) match, you can significantly increase your retirement savings and potentially retire comfortably. So if your employer offers a 401(k) match, take advantage of it and start saving today!

References:

“401(k) Contribution Limits for 2021,” IRS.gov, accessed September 15, 2021.

“The Power of Compounding,” Investor.gov, accessed September 15, 2021.

“Vesting,” Investopedia, accessed September 15, 2021.

Understanding Secure Act 2.0

The SECURE 2.0 Act of 2022 is a legal framework that aims to improve retirement savings options, such as 401(k)s and 403(b)s, in the United States. It is built on the foundation of the SECURE Act of 2019 and was signed into law by President Joseph R. Biden on December 29, 2022, as a part of the Consolidated Appropriations Act (CAA) of 2023. The SECURE 2.0 Act comprises two pieces of legislation, one from the House of Representatives (H.R. 2954) and one from the U.S. Senate (S. 1770), which were consolidated into the CAA omnibus budget bill as Division T (SECURE 2.0 Act of 2022).

The SECURE 2.0 Act consists of 92 new provisions that promote savings, increase incentives for businesses, and provide more flexibility to those saving for retirement. The provisions include automatic 401(k) enrollment, an increase in the age for taking required minimum distributions (RMDs), significant tax benefits for employers, and more. The legislation in both chambers received broad bipartisan support, with 103 sponsors of H.R. 2954 consisting of 55 Democrats and 48 Republicans and six Republicans and five Democrats co-sponsoring S. 1770.

The SECURE 2.0 Act aims to achieve three goals: encouraging people to save more for retirement, improving retirement rules, and reducing the employer cost of setting up a retirement plan. Some of the provisions went into effect on January 1, 2023, while others will take effect in 2024, 2025, and beyond. For example, Section 101 of the SECURE 2.0 Act mandates employers to automatically enroll eligible employees in new 401(k) or 403(b) plans, starting in 2025. The contribution amount is at least 3% but no more than 10%, which escalates by 1% per year up to a minimum of 10% and a maximum of 15%. While Section 107 of the SECURE 2.0 Act increases the required minimum distribution age to 73, effective from January 1, 2023, and to 75 beginning in 2033.

Other provisions of the SECURE 2.0 Act include changes to catch-up contribution limits, expanded access to retirement funds, and an increased amount for qualified longevity annuity contracts (QLACs) from $125,000 to $200,000. The Act also allows participants to access up to $1,000 from retirement savings for emergency personal or family expenses without paying the 10% early withdrawal penalty, permits employees to set up a Roth emergency savings account with up to $2,500 per participant, and allows survivors of domestic abuse to withdraw the lesser of $10,000 or 50% of their retirement account without penalty.

The effective date of the provisions in the SECURE 2.0 Act varies, with some taking effect immediately, while others will take effect in 2023, 2024, or beyond. For instance, automatic retirement plan enrollment will start in 2025, while the increase in the age for RMDs from 72 to 73 began on January 1, 2023.

The Lost Decade: How Index Annuities Could Have Protected Your Retirement Savings

The Lost Decade: How Index Annuities Could Have Protected Your Retirement Savings

The 10 years from 2001-2010, known as the “Lost Decade,” were a challenging time for investors. Key U.S. stock market indices either posted negligible returns or suffered negative returns. The S&P 500 Index closed down 4.74% at the end of this time period, causing many individuals to lose a significant portion of their retirement savings.

However, today’s index annuity could have protected your annuity’s value from the sharp market declines of the early 2000s and 2008. An index annuity is a type of annuity that earns interest based on the performance of a specific index, such as the S&P 500. The renewing 5% index rate cap means that the maximum potential of annual interest earned is based on index performance and can change each year.

For example, from 2003 to 2007 and in 2009 and 2010, the index annuity with a renewing 5% index rate cap would have provided growth potential during the positive years. This means that investors could have earned interest on their principal investment during these years, without subjecting it to the risks associated with the stock market.

Index annuities are a popular choice for retirees who want to protect their retirement savings while still earning interest. They offer a level of safety that traditional stocks and mutual funds cannot provide. Because they are tied to specific indices, they are not subject to the volatility of individual stocks or mutual funds. This means that investors can enjoy the potential for growth without having to worry about market fluctuations.

It’s important to note that past performance is not a guarantee of future results. However, index annuities have a track record of providing steady returns, even during volatile market conditions. They are an excellent option for retirees who want to protect their retirement savings while still earning interest.

In conclusion, the Lost Decade was a difficult time for investors, but index annuities could have protected your retirement savings from market declines. With a renewing 5% index rate cap, investors could have earned interest during positive years without subjecting their principal investment to market risks. Index annuities offer a level of safety that traditional stocks and mutual funds cannot provide, making them an excellent option for retirees who want to protect their retirement savings while still earning interest.

Don't Leave Your Tax Burden Behind in Retirement:

Don’t Leave Your Tax Burden Behind in Retirement: A Guide to Planning Ahead

As you approach retirement, you may be thinking about the relaxing days ahead, spending time with family and friends, and pursuing hobbies and interests that you didn’t have time for during your working years. However, one thing that you may not be considering is your tax burden in retirement. Many retirees are surprised to find that they still have to pay taxes on their income, even if they are no longer working full-time. In this article, we’ll explore the importance of tax planning in retirement and provide tips to help you avoid leaving your tax burden behind.

Why Tax Planning is Important in Retirement

The first thing you need to understand is that retirement does not mean an end to taxes. In fact, you may face a higher tax burden in retirement than you did while working. This is because many retirees have income from various sources, such as pensions, Social Security benefits, investments, and rental properties. Each of these sources of income may be subject to different tax rates and rules, so it’s essential to understand how they will impact your overall tax liability.

Another reason why tax planning is crucial in retirement is that you may have more control over your income and expenses than you did while working. For example, you may be able to adjust your retirement account distributions or delay taking Social Security benefits to reduce your taxable income. You may also be able to take advantage of tax deductions and credits that were not available to you while employed.

Tips for Planning Your Retirement Taxes

Now that you know why tax planning is essential in retirement, let’s discuss some practical tips to help you avoid leaving your tax burden behind.

Understand Your Retirement Income Sources

The first step in tax planning is to understand the various sources of income you will have in retirement. This may include Social Security benefits, pension income, withdrawals from retirement accounts, and investment income. Each of these income sources may be taxed differently, so it’s crucial to understand how they will impact your overall tax liability.

Consider Delaying Social Security Benefits

One way to reduce your taxable income in retirement is to delay taking Social Security benefits. You can begin taking Social Security benefits as early as age 62, but if you delay taking benefits until your full retirement age (currently age 66 or 67, depending on your birth year), you can receive a higher monthly benefit. If you delay taking benefits until age 70, your monthly benefit will be even higher. By delaying Social Security benefits, you can reduce your taxable income and increase your overall retirement income.

Monitor Your Retirement Account Withdrawals

If you have traditional retirement accounts, such as a 401(k) or IRA, withdrawals from these accounts are generally taxable. However, if you withdraw too much from your retirement accounts in a given year, you may push yourself into a higher tax bracket. To avoid this, it’s important to monitor your retirement account withdrawals and adjust them as needed to avoid unnecessary taxes.

Take Advantage of Tax Deductions and Credits

Even in retirement, you may be eligible for tax deductions and credits that can reduce your overall tax liability. For example, you may be able to deduct medical expenses or charitable contributions. You may also be eligible for the Earned Income Tax Credit if you have low income in retirement.

Work with a Tax Professional

Finally, it’s a good idea to work with a tax professional who can help you navigate the complex tax rules and regulations in retirement. A tax professional can help you identify tax-saving strategies and ensure that you are taking advantage of all available deductions and credits.

Conclusion

Retirement should be a time to relax and enjoy life, but it’s important not to leave your tax burden behind. By understanding your retirement income sources, delaying Social Security benefits, monitoring your retirement account withdrawals, taking advantage of tax deductions and credits, and working with a tax professional, you can reduce your tax burden and enjoy a more comfortable retirement.

IRA Wealth Transfer Strategy: Maximizing Your Retirement Legacy

IRA Wealth Transfer Strategy: Maximizing Your Retirement Legacy

As you approach retirement, you may be thinking about how you can leave a legacy for your loved ones. One strategy to consider is an IRA wealth transfer plan. An IRA, or individual retirement account, can be a powerful tool for building wealth and transferring assets to your heirs.

What is an IRA?

An IRA is a tax-advantaged retirement savings account that allows you to save and invest money for your retirement years. There are two main types of IRAs: traditional and Roth. With a traditional IRA, contributions may be tax-deductible, and earnings grow tax-deferred until you withdraw them in retirement. With a Roth IRA, contributions are made with after-tax dollars, but earnings and withdrawals are tax-free.

Why consider an IRA wealth transfer plan?

One of the benefits of an IRA is that it allows you to name a beneficiary who will inherit the account when you pass away. This can be an effective way to transfer wealth to your heirs, as they will receive the funds without having to go through probate. Additionally, if you name your spouse as the beneficiary, they can roll the IRA into their own account and continue to defer taxes on the investments.

However, it’s important to plan ahead and consider the impact of taxes on your legacy. If you leave an IRA to a non-spouse beneficiary, they will have to take required minimum distributions (RMDs) based on their own life expectancy. This means that they will have to withdraw a certain amount each year, which will be subject to income tax. Depending on the size of the IRA and the beneficiary’s tax bracket, this could result in a significant tax burden.

How can you maximize your IRA legacy?

One strategy to consider is a stretch IRA. This involves naming a younger beneficiary, such as a child or grandchild, who can take distributions over their own life expectancy. This can potentially stretch out the tax-deferred growth of the IRA over several decades, minimizing the tax impact. Additionally, you can consider setting up a trust to hold the IRA, which can provide greater control and protection for your heirs.

Another option is to convert traditional IRA funds to a Roth IRA. This can be a smart move if you expect your beneficiaries to be in a higher tax bracket in the future. By paying taxes on the conversion now, you can ensure that the funds will be tax-free for your heirs in the future. Keep in mind that a Roth conversion can have significant tax implications, so it’s important to consult with a financial advisor or tax professional before making this decision.

Conclusion

An IRA wealth transfer plan can be a powerful tool for leaving a legacy for your loved ones. By considering your options and planning ahead, you can maximize the tax benefits and ensure that your assets are transferred according to your wishes. As with any financial decision, it’s important to consult with a qualified professional to ensure that you are making the best choice for your individual circumstances.

SEO friendly title: Maximizing Your Retirement Legacy with an IRA Wealth Transfer Plan

"Assessing Your Risk Tolerance: How Much Investment Risk Should You Take for a Comfortable Retirement?"

“Assessing Your Risk Tolerance: How Much Investment Risk Should You Take for a Comfortable Retirement?”

As you plan for retirement, one of the most important decisions you’ll need to make is how much investment risk to take on. Investing involves uncertainty, and the tradeoff between risk and reward can be daunting. How can you determine how much risk you should take on? That’s where understanding your risk tolerance comes in.

What is Risk Tolerance?

Risk tolerance is the degree of volatility or uncertainty an investor is willing to accept in their investments. It is influenced by a variety of factors, including age, income, financial goals, investment time horizon, and personal temperament. Some investors are comfortable with high levels of risk, while others prefer low-risk investments. Understanding your risk tolerance is critical to creating a portfolio that aligns with your goals and comfort level.

Assessing Your Risk Tolerance

There are several ways to assess your risk tolerance. One approach is to complete a risk tolerance questionnaire, which is designed to evaluate your willingness to accept volatility in your investments. These questionnaires typically ask a series of questions about your investment goals, time horizon, and financial situation. The results can help you determine the appropriate level of risk for your portfolio.

Another approach is to work with a financial advisor who can help evaluate your risk tolerance and recommend investments that align with your goals and comfort level. A financial advisor can also help you create a diversified portfolio that balances risk and return.

The Importance of Asset Allocation

Once you’ve assessed your risk tolerance, it’s time to create a portfolio that aligns with your goals. One of the most important decisions you’ll need to make is how to allocate your assets. Asset allocation refers to the percentage of your portfolio invested in different asset classes, such as stocks, bonds, and cash.

Asset allocation is critical because it can have a significant impact on your portfolio’s performance. Studies have shown that asset allocation can explain up to 90% of a portfolio’s returns over time. A diversified portfolio that includes a mix of asset classes can help reduce risk and volatility, while still providing the potential for growth.

Balancing Risk and Reward

Ultimately, the amount of investment risk you take on depends on your financial goals, time horizon, and risk tolerance. It’s important to balance risk and reward, and avoid taking on too much risk or too little risk. Taking on too much risk can lead to significant losses, while taking on too little risk can result in lower returns and the possibility of outliving your savings.

As you plan for retirement, it’s important to assess your risk tolerance and create a portfolio that aligns with your goals and comfort level. By working with a financial advisor and focusing on asset allocation, you can create a diversified portfolio that balances risk and reward and provides a comfortable retirement.

SEO keywords: risk tolerance, investment risk, retirement, asset allocation, financial advisor, portfolio, volatility, diversification, risk and reward, returns.

References:

“Risk Tolerance: What It Is and Why It Matters,” Investopedia, https://www.investopedia.com/terms/r/risktolerance.asp.

“Asset Allocation and Diversification,” Investor.gov, https://www.investor.gov/introduction-investing/investing-basics/glossary/asset-allocation-diversification.

“Balancing Risk and Return,” Vanguard, https://investor.vanguard.com/investing/how-to-invest/balancing-risk-and-return.

The Shocking Reality: Nearly Half of Baby Boomers Have No Retirement Savings

The Shocking Reality: Nearly Half of Baby Boomers Have No Retirement Savings

As the baby boomer generation reaches retirement age, a shocking reality is starting to come to light: nearly half of them have no retirement savings. According to a report by the Insured Retirement Institute, 45% of baby boomers have no retirement savings at all. This is a concerning trend that is affecting not only the boomers themselves, but also the economy at large.

One of the reasons for this lack of retirement savings is the decline in traditional pension plans. In the past, many companies provided their employees with defined benefit pension plans, which guaranteed a certain amount of income in retirement. However, these plans have become less common in recent years, leaving many baby boomers without a reliable source of retirement income.

Another factor is the rising cost of healthcare. As baby boomers age, they are more likely to face health problems that require expensive medical care. This can quickly eat away at any retirement savings they may have, leaving them with little to live on.

Furthermore, many baby boomers are still paying off their mortgages and other debts, which can make it difficult to save for retirement. They may also be supporting adult children or elderly parents, putting additional strain on their finances.

So, what can be done to address this issue? One solution is for baby boomers to work longer and delay retirement. This can provide them with additional income and give them more time to save for retirement. It can also help to reduce the strain on Social Security, which is facing its own financial challenges.

Another solution is to encourage baby boomers to save more aggressively for retirement. This can be done through education and financial planning services. Many baby boomers may not realize how much they need to save for retirement or how to best invest their savings. By providing them with the knowledge and tools they need, they can make better decisions about their finances and prepare for retirement.

In conclusion, the fact that nearly half of baby boomers have no retirement savings is a concerning trend that needs to be addressed. With the right solutions, however, it is possible to help these individuals prepare for retirement and ensure their financial security in their golden years.

References:

Insured Retirement Institute. (2019). Boomer Expectations for Retirement 2019. Retrieved from https://www.myirionline.org/docs/default-source/research/boomer-expectations-for-retirement-2019.pdf

Social Security Administration. (2021). Status of the Social Security and Medicare Programs. Retrieved from https://www.ssa.gov/OACT/TR/index.html

Good credit score will cost you more under Biden's new mortgage rule

Good Credit Score Will Cost More Under Biden’s New Mortgage Rule: What You Need to Know

The Biden administration recently announced new mortgage rules that will have an impact on borrowers with good credit scores. While the changes are aimed at addressing racial and economic disparities in the housing market, they will also affect those who have worked hard to maintain good credit.

Under the new rules, lenders will have to consider a borrower’s debt-to-income ratio, instead of just their credit score, when underwriting a mortgage. This means that borrowers with higher credit scores and more debt may face higher interest rates and stricter lending standards.

Why the Change?

The Biden administration is seeking to address the racial and economic disparities in the housing market. Studies have shown that Black and Hispanic borrowers are more likely to be denied mortgages than white borrowers with similar credit profiles. The new rules aim to address this by taking into account a borrower’s ability to repay the loan, rather than just their credit score.

The administration is also concerned about the housing market’s stability. Lenders have been offering mortgages with low down payments and lenient lending standards, which has led to a rise in defaults and foreclosures. By tightening lending standards, the administration hopes to prevent another housing crisis.

What Does This Mean for Borrowers?

If you have a good credit score but a high debt-to-income ratio, you may find it more difficult to secure a mortgage. Even if you do qualify for a loan, you may face higher interest rates and stricter lending standards.

This is because lenders will have to factor in your debt-to-income ratio when evaluating your application. Your debt-to-income ratio is the amount of debt you have compared to your income. If you have a lot of debt, you may not be able to afford the monthly mortgage payments, even if you have a high credit score.

To qualify for a mortgage under the new rules, you will need to have a debt-to-income ratio of 43% or lower. This means that your monthly debt payments, including your mortgage, should not be more than 43% of your monthly income.

What Can You Do?

If you have a high debt-to-income ratio, there are a few things you can do to improve your chances of qualifying for a mortgage:

Pay Down Your Debt: If you have high credit card balances or other debt, consider paying it down before applying for a mortgage. This will lower your debt-to-income ratio and improve your chances of qualifying for a loan.

Increase Your Income: If you have a low income, consider taking on a second job or asking for a raise at your current job. This will increase your income and improve your debt-to-income ratio.

Shop Around: Different lenders have different lending standards, so it’s important to shop around and find the lender that best fits your needs. You may also want to consider working with a mortgage broker, who can help you find the best loan for your situation.

In Conclusion

The new mortgage rules under the Biden administration will have an impact on borrowers with good credit scores and high debt-to-income ratios. While the changes are aimed at addressing racial and economic disparities in the housing market, they may also make it more difficult for some borrowers to secure a mortgage. If you’re in this situation, it’s important to take steps to improve your debt-to-income ratio and shop around for the best loan.

New Rules on Taxation on the Sale of a Home: What You Need to Know

New Rules on Taxation on the Sale of a Home: What You Need to Know

Selling a home can be a bittersweet experience, but it’s important to keep in mind that there are taxation rules involved in this process. Recently, there have been some new regulations put in place that may affect the way you handle the sale of your home. In this article, we’ll take a closer look at those new rules and what they mean for you as a homeowner.

First, it’s important to understand the basics of home sale taxation. When you sell a home, you may be subject to capital gains tax on any profit you make from the sale. This tax applies to any property that is not your primary residence, such as a rental property or vacation home. However, there are some exemptions that may apply if you meet certain criteria.

Now, let’s take a look at the new rules that have been put in place. In December 2017, a tax bill was signed into law that made significant changes to the way home sale taxation works. Under the new law, the capital gains tax exemption for the sale of a primary residence remains in place. This means that if you sell your primary residence and make a profit, you may be able to exclude up to $250,000 (or $500,000 for married couples filing jointly) of that profit from capital gains tax.

However, there are some changes that could affect homeowners. First, the law now requires that you must have lived in the property for at least five of the past eight years in order to qualify for the exemption. This means that if you sell a home that you have lived in for less than five years, you may be subject to capital gains tax on any profit you make.

Another change to be aware of is the way that the deduction for mortgage interest works. Under the new law, the deduction for mortgage interest is limited to interest on up to $750,000 of mortgage debt. This means that if you have a mortgage that exceeds this amount, you may not be able to deduct all of the interest paid on your tax return.

So, what does this all mean for homeowners? The biggest takeaway is that it’s important to plan ahead if you’re considering selling your home. If you’ve lived in the property for less than five years, you may want to consider waiting until you meet the eligibility requirements for the primary residence exemption. Additionally, if you have a large mortgage, you may need to adjust your budget to account for the fact that you may not be able to deduct all of the interest paid.

In conclusion, the new rules on taxation on the sale of a home may seem daunting, but with a little planning and preparation, you can navigate the process with confidence. Remember to consult with a tax professional or financial advisor if you have any questions or concerns about how these rules may affect you.

SEO Title: New Rules on Taxation on the Sale of a Home: What You Need to Know

Keywords: home sale taxation, capital gains tax, primary residence exemption, mortgage interest deduction, tax bill, eligibility requirements, tax professional, financial advisor

Understanding the average pension in the USA is crucial.

As retirement planning becomes an increasingly significant concern for many people, understanding the average pension in the USA is crucial. This article will explore what the average pension in the USA is, why it is important, and how it varies by state.

What is a Pension?

A pension is a form of retirement plan that provides a fixed income for life once an employee retires. Employers may offer pensions as a benefit to their employees, and employees may also contribute to their pensions. Pensions are typically funded by the employer, and employees may also make contributions to their pensions through salary reductions.

The Importance of Knowing the Average Pension in the USA

Understanding the average pension in the USA is critical for several reasons. Firstly, it helps individuals gauge their retirement readiness and plan their retirement savings goals. It also helps employers benchmark their pension plans against industry standards to ensure they are competitive in the workforce. Additionally, policymakers can use this information to assess the effectiveness of retirement policy initiatives and identify areas where improvements are needed.

What is the Average Pension in the USA?

According to a report by the National Institute on Retirement Security, the average pension in the USA is $9,135 per year. However, this figure varies significantly by state. For example, the average pension in Alaska is $22,346 per year, while the average pension in Florida is $6,045 per year.

Factors Affecting the Average Pension in the USA

Several factors affect the average pension in the USA, including the cost of living, the size of the workforce, and the length of time employees have worked for their employers. States with a higher cost of living, such as Alaska and Hawaii, typically have higher pension payouts. States with a larger workforce and a more significant number of retirees, such as California and New York, tend to have higher average pensions. Finally, employees who have worked for their employers for a more extended period typically have higher pension payouts than those who have only worked for a short time.

Conclusion

In conclusion, the average pension in the USA is $9,135 per year, but this figure varies significantly by state. Understanding the average pension in the USA is crucial for individuals, employers, and policymakers alike. By understanding the factors that affect pension payouts, workers can make informed decisions about their retirement savings goals. Employers can benchmark their pension plans against industry standards, and policymakers can use this information to improve retirement policy initiatives. Overall, knowledge of the average pension in the USA is essential for anyone planning for their retirement future.

SEO Friendly Title: What is the Average Pension in the USA and Why Does it Matter?

Health Conditions and Home Foreclosure:

Title: The Impact of Developing Health Conditions on Home Foreclosure: A Comprehensive Guide for Financial Planning

Foreclosures can be a nightmare for homeowners. The process of losing a home can be stressful and emotional, and can have long-lasting financial repercussions. In recent years, the link between health conditions and home foreclosure has become more apparent. This article will provide a comprehensive guide for financial planning in the face of developing health conditions and the potential for home foreclosure.

The Connection Between Health Conditions and Home Foreclosure

Health conditions can have a significant impact on a person’s ability to maintain their home and pay their mortgage. For example, a serious illness or injury can result in high medical bills and a loss of income due to missed work. A chronic health condition can lead to ongoing medical expenses, which may make it difficult to keep up with mortgage payments. Mental health conditions, such as depression or anxiety, can also have a negative impact on a person’s ability to manage their finances.

In addition to these direct impacts, health conditions can also lead to other financial challenges that can ultimately result in home foreclosure. For example, a person with a chronic illness may find it difficult to work full-time, which can result in a reduced income. This may make it difficult to keep up with all of their bills, including their mortgage payments.

Similarly, if a person with a health condition is unable to work at all, they may have to rely on disability benefits or other forms of assistance to make ends meet. These benefits may not be enough to cover all of their expenses, including their mortgage payments, leading to financial difficulties.

Overall, health conditions can have a significant impact on a person’s financial situation, which can ultimately lead to home foreclosure.

Financial Planning for Homeowners with Health Conditions

If you or someone you know is facing a health condition and the potential for home foreclosure, there are steps you can take to protect your financial future. The following tips can help you to create a financial plan that will help you to weather the storm and avoid foreclosure:

Seek financial advice: If you are facing a health condition and the potential for foreclosure, it is important to seek the advice of a financial professional. They can help you to understand your options and create a plan that will help you to avoid foreclosure.

Communicate with your lender: If you are struggling to make your mortgage payments due to a health condition, it is important to communicate with your lender. They may be able to offer you a loan modification, forbearance, or other forms of assistance that can help you to stay in your home.

Look for assistance programs: There are many government and non-profit programs that can provide financial assistance to homeowners who are struggling to make their mortgage payments. Look for programs in your area that may be able to help you.

Create a budget: Creating a budget is an important step in managing your finances when facing a health condition and the potential for foreclosure. A budget can help you to prioritize your expenses and ensure that you are able to make your mortgage payments.

Explore selling options: If you are unable to keep up with your mortgage payments, it may be necessary to explore selling options. This could include selling your home and downsizing, or working with your lender to explore a short sale.

Conclusion

Developing health conditions can have a significant impact on a person’s financial situation, including their ability to keep their home. However, with the right financial planning and support, it is possible to avoid foreclosure and protect your financial future. By seeking financial advice, communicating with your lender, looking for assistance programs, creating a budget, and exploring selling options, you can create a plan that will help you to weather the storm and avoid foreclosure.

Medical Bankruptcy: What You Need to Know

Medical Bankruptcy: What You Need to Know

Medical bankruptcy is a term that refers to the inability of an individual or a business to pay for their medical bills. It is a growing problem in the United States, where healthcare costs have risen significantly in recent years. In fact, according to a study conducted by the American Journal of Public Health, medical bills are the leading cause of bankruptcy in the United States. In this article, we will discuss the causes, consequences, and options available for those facing medical bankruptcy.

Causes of Medical Bankruptcy

The high cost of healthcare is the primary cause of medical bankruptcy. According to a study published in the American Journal of Medicine, medical bills account for 62% of all bankruptcies in the United States. This is because many people do not have health insurance or have inadequate insurance coverage. Even those with insurance are often faced with high co-pays, deductibles, and out-of-pocket expenses. In addition, many medical treatments are not covered by insurance, leaving patients with large bills to pay.

Another cause of medical bankruptcy is the loss of income due to illness or injury. When people are unable to work due to their medical condition, they lose their source of income and may not be able to pay their bills. This can lead to financial hardship and bankruptcy.

Consequences of Medical Bankruptcy

The consequences of medical bankruptcy can be devastating. Not only does it affect an individual’s financial stability, but it can also impact their mental and physical health. Medical bankruptcy can lead to:

Loss of assets: People who file for bankruptcy may lose their homes, cars, and other assets.

Damaged credit score: Bankruptcy can stay on a person’s credit report for up to 10 years, making it difficult to obtain credit or loans in the future.

Stress and anxiety: The financial strain of medical bills and bankruptcy can cause stress and anxiety, which can impact a person’s overall health.

Delayed medical treatment: People who are unable to pay for medical bills may delay or forego necessary medical treatment, which can lead to further health complications.

Options for Those Facing Medical Bankruptcy

If you are facing medical bankruptcy, there are options available to help you manage your debt. These include:

Negotiating with healthcare providers: Many healthcare providers are willing to negotiate payment plans or offer discounts to patients who are unable to pay their bills in full.

Applying for financial assistance: Some hospitals and healthcare organizations offer financial assistance programs for low-income patients.

Filing for bankruptcy: Bankruptcy can provide a fresh start for those who are overwhelmed by medical debt. It can help eliminate or reduce unsecured debt, such as medical bills.

Seeking legal assistance: It may be helpful to seek the assistance of a bankruptcy attorney who can guide you through the bankruptcy process and help you make informed decisions.

Conclusion

Medical bankruptcy is a growing problem in the United States, affecting individuals and businesses alike. The high cost of healthcare and the loss of income due to illness or injury are the primary causes. The consequences of medical bankruptcy can be devastating, but there are options available to help manage the debt. By negotiating with healthcare providers, applying for financial assistance, or filing for bankruptcy, individuals can take steps to regain their financial stability and focus on their health.

Is Cruise Ship Living a Cheaper Option for Seniors Than Assisted Living?

Is Cruise Ship Living a Cheaper Option for Seniors Than Assisted Living?

As the number of seniors in the United States continues to rise, so does the cost of assisted living. According to the Genworth 2020 Cost of Care Survey, the average cost of a private room in an assisted living facility is $4,300 per month, while a semi-private room costs $3,800. These costs are often too high for seniors on a fixed income, leading many to explore alternative options, such as cruise ship living.

Cruise ship living has become a popular alternative for seniors who want to travel and enjoy the amenities of a retirement community at a lower cost than assisted living. While the idea of living on a cruise ship may seem unusual, it can be an affordable and enjoyable option for seniors.

The Cost of Cruise Ship Living

The average cost of a cruise can vary depending on the length of the voyage, the type of cabin, and the cruise line. However, many seniors find that the cost of a cruise is comparable to the cost of assisted living. For example, a 10-day cruise can cost around $3,000 per person, which includes food, entertainment, and most of the activities on board. This cost is comparable to a month’s rent in an assisted living facility.

Furthermore, seniors who choose to live on a cruise ship full-time can often negotiate long-term rates that are more affordable than traditional assisted living facilities. Some cruise lines even offer retirement communities on board that are designed specifically for seniors.

Benefits of Cruise Ship Living

Cruise ship living offers numerous benefits that are not available in traditional assisted living facilities. For instance, seniors can wake up in a new location every day, enjoy gourmet meals, and participate in activities such as dancing, fitness classes, and enrichment programs. They can also enjoy the company of other passengers, forming new friendships and exploring new destinations together.

Seniors who live on a cruise ship also have access to 24-hour medical care, which can be especially important for those with chronic health conditions. While some may worry about the safety of living on a ship, cruise lines have strict safety protocols in place to ensure the wellbeing of their passengers.

Drawbacks of Cruise Ship Living

While cruise ship living can be an attractive option for some seniors, it is not without its drawbacks. For example, living on a ship requires a significant amount of mobility, which may not be possible for seniors with mobility issues. Additionally, living on a ship means living in a small cabin with limited space, which can be challenging for some individuals.

Furthermore, cruise ship living often means being away from family and friends for extended periods of time. It can also be expensive to bring guests on board, which can limit the amount of time seniors are able to spend with loved ones.

Conclusion

Cruise ship living can be an affordable and enjoyable alternative to traditional assisted living facilities for seniors. While it may not be suitable for everyone, those who are mobile and enjoy travel may find that cruise ship living offers a unique and fulfilling retirement lifestyle. With careful planning and research, seniors can determine if cruise ship living is the right option for them.

SEO Title: Is Cruise Ship Living Cheaper Than Assisted Living for Seniors?

Index Universal Life

IUL Mysteries

Myths & Facts Explained!

We’ve been working at our best to ensure our clients’ financial future, and to provide the best financial services possible. We stand for quality and credibility, so you could be sure about our work.

TOP-RATED FINANCIAL NEWS

Don’t have time to read, you can listen to our podcast at: https://www.redzonetoolbox.com/

Have a topic you would like more clarity on send us an email: info@gambrellfinancial.com

An IUL Will Outperform The Stock Market?

An IUL Will Outperform The Stock Market? *Ahh NO IT WILL NOT*

An IUL or Whole Life Insurance plan will not outperform the stock market!

Life Insurance products, when structured properly can be an awesome tool to grow tax-free retirement income, but it’s not a replacement for stock market growth!